- Research into cyclical and structural changes, as well as their consequences and impact on the sector's recovery timeline

- Research into the benefits of office and work-from-home, including KPIs such as productivity, engagement, and employee creativity. Also, how company culture and branding is transforming under the influence of remote workplaces

- Search for the optimal flexible workplace model, consisting of traditional and home office. It is designed to increase employee satisfaction and productivity, as well as company profitability

- Forecasts for the future of the office real estate sector. They are based on analysis of factors that significantly impact the construction sector - economics, geodemographics, technology, social shifts, and the political landscape. Changes in behavioral patterns that will influence decision-making are also taken into account

PART 1. COVID-19 PANDEMIC'S IMPACT ON THE OFFICE REAL ESTATE SECTOR

COVID-19 is undermining established economic processes and creating factors that directly affect the office real estate sector. They can be divided into:- Cyclical, whose impact is relatively short-term

- Structural, which will persist for many years

The cyclical factors include:

- job cuts

- increased vacant office space

- and, as a result, lower rental rates

Structural factors include, for example, the increased share of employees who will regularly work from home (WHF - work from home).

The first part of the study examines their combined impact on the sector, as well as proposes 3 scenarios that illustrate probable and/or possible results based on available information.

The first part of the study examines their combined impact on the sector, as well as proposes 3 scenarios that illustrate probable and/or possible results based on available information.

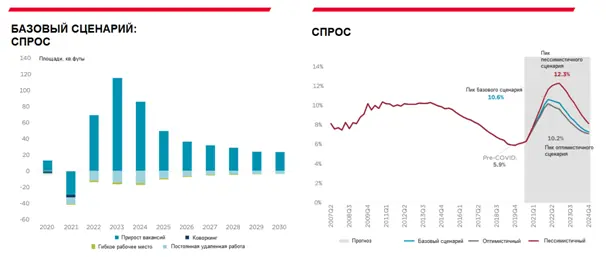

Rental rates are forecast to reach their lowest point in Q1 2022, after which they are expected to rise to pre-crisis levels by 2025. COVID-19 requires social distancing from society in the near future. Therefore, the long-standing trend toward densification, where companies consumed less space per office employee, is a thing of the past.

KEY FINDINGS

- The trend toward mass transition to work from home will be offset by post-pandemic economic growth, population growth, and increasing demand for services that can only be provided in a traditional office. The forecast horizon is 10 years

- On a global scale, the commercial real estate sector will suffer colossal damage exceeding the damage from the Global Financial Crisis of 2008. For comparison, in 2008, 85 million sq. ft. became available worldwide, and in the period from Q2 2020 to Q3 2021 - 95 million sq. ft. Europe, Canada, and the US will bear the main impact

- Global supply of office space offered for rent will grow from 10.9% pre-crisis (Q4 2019) to 15.6% in Q2 2022. According to forecasts, global rent will decrease by 10.9% from peak to minimum from Q2 2020 to Q1 2022

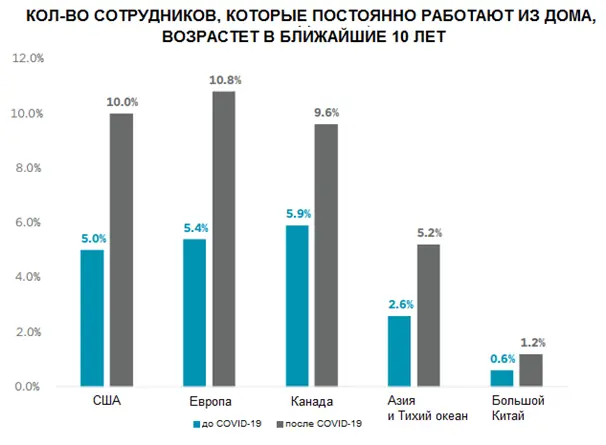

- Of the 95.8 million sq. ft. available, 82% are related to cyclical factors, namely job losses and coworking impact. The remaining 18% are related to structural factors. In particular, this is the assumption that the share of both permanent remote employees and flexible employees - those who work remotely part-time - will increase. The share of people permanently working from home in the US and Europe is expected to increase from ~5-6% pre-COVID to ~10-11% post-COVID, and the share of agile workers increases from ~32-36% to just under 50%. These structural impacts are significantly lower in the Asia-Pacific region and Greater China, where remote work is less common

- COVID-19 requires social distancing from society and disrupts the long-standing trend of densification, when less and less space was allocated per employee in the office. However, it is still unclear how long the structural reversal of densification - de-densification - will last. At minimum, Cushman & Wakefield believe that densification will stop and that methods allowing for distancing, such as flexible work and shift work, will increase

- De-densification can compensate for some of the loss in demand for office real estate caused by transitioning employees to work from home, even completely neutralizing it. For example, expanding occupied space by 50% per worker relative to the pre-COVID period completely neutralizes the expected negative effects of increased remote work in the US by 2030

- As the economy and employment recover, the global office sector will start renting more offices in Q1 2022 and reducing supply. It will return to pre-crisis levels of 11% by 2025

- On a global scale, rent will start rising in Q1 2022 and return to pre-crisis levels in 2025

5-YEAR OUTLOOK (BASE SCENARIO)

RESEARCH OVERVIEW

The COVID-19 pandemic has seriously affected commercial real estate through various aspects. Some were quite predictable, while others are not so simple. One of the most widely discussed topics is:- The future of office real estate

- The role it will play in the post-pandemic world

- How employment strategies will develop further

This study evaluates the potential impact of several forces that could affect demand for office real estate - and, consequently, the fundamental operating principles of this sector. Cushman & Wakefield tried to cover the widest range of scenarios based on available data. However, they do not deny the unprecedented level of uncertainty in today's outlook.

In terms of cyclical changes, both the consequences of people losing jobs during and after the economic downturn, as well as the possibility of reduced demand for coworking, were taken into account. The effect is insignificant since in most cities - and certainly at the regional level - coworking occupies a small share of total commercial space. However, in selected markets, combining traditional and home office will likely lead to increased supply of office space.

Structurally, it is assumed that employment forms and decision-making processes may change. Moreover, some of these changes may become permanent or at least long-term. This study focuses on the impact of the factor of increased share of employees working from home on demand for office space. It also evaluates the significance of this impact relative to various assumptions. The study does not include impacts at a single country level that may arise from a more geographically distributed workforce, long-term urbanization, or shifts in preferences regarding central or suburban office locations.

The pandemic forced organizations to allow widespread work-from-home. The results showed that flexible remote work yields benefits. Workers themselves prefer this type of employment and continue to advocate for the right to work this way. Although many also want to spend at least some time in the office. Additionally, leaders report that they plan to implement more flexible working methods, including the ability to work from home in the post-COVID period.

However, this does not apply to all companies. Although working from home has its advantages, the traditional workplace in the office is crucial for both employers and employees. Cushman & Wakefield believe that the future workplace ecosystem is a mix of traditional office spaces, home offices, and semi-public spaces. It is very unlikely that any one option will predominate, especially for companies that rely on innovation, knowledge dissemination, and creative approaches to create value and revenue. Cities are the epicenter of such phenomena.

Furthermore, despite its advantages, remote work also creates certain difficulties for companies and their employees. For example, opportunities for training, mentoring, and communication worsen. According to Gensler's 2019 study, the main reason workers prefer to work in the office is simply social connections and team bonding. During COVID-19, this preference was confirmed by data from more than 60,000 respondents from more than 100 companies worldwide. Therefore, it is not surprising that 65% of respondents worldwide said they would prefer to work from home more often than before COVID-19. In the Asia-Pacific region (excluding Greater China), Canada, Europe, and the US, this share was approximately 64-65%, while in Greater China it was 30%.

In the Asia-Pacific region, developing markets had a 40% share of such workers, while developed economies had just under 58%. It should be noted that between 35% of workers (mainly in developed economies) and 70% in Greater China do not want to change their attitude toward remote work in the long term.

These figures generally align with Cushman & Wakefield's estimates of the peak potential for remote jobs in each region. These estimates suggest that approximately 60% of jobs worldwide could be remote. This data outlines the potential upper limit for long-term structural changes that may occur over the next decade. This potential has not yet been realized. Over time, it is possible that current preferences will disappear as society returns to a more normal work environment and pandemic concerns subside.

Large-scale surveys of both line employees and managers show that most people want to be in the office at least a few days a week. But at the same time, they want some changes, including the ability to work from home; social distancing in the office, in particular more single desks and more personal space. Therefore, even with a combined increase in the share of employees who work remotely, not all companies plan to reduce their office space leases.

General forecasts are, of course, adjusted for regional characteristics. For example, for developing markets in the Asia-Pacific region and mainland China, growth in demand for office space is very likely due to the increased share of services that can only be provided in the office, as well as high population density, especially in China and India. Moreover, these regions were least affected by structural changes. In the base scenario, net demand for office space from 2022 to 2030 (the period during which negative cyclical effects are most likely to disappear) is only 4.5% lower in the Asia-Pacific region and 2.9% lower in Greater China than expected without COVID-19.

In the West, remote work has greater potential to undermine demand for office space. According to our estimates, from 2022 to 2030, in accordance with the base scenario, the demand impact will range from -14.8% in Canada to -15.8% in the US and -17.4% in Europe. Generally, these regions experience greater impact from an aging workforce and the associated decrease in overall employment and increase in employees who work remotely on a permanent basis. This is a significant obstacle to recovering demand for office space. Pre-COVID, the share of remote employees was 5-6% and it is expected to double to 10-11% by 2030.

Although short-term prospects vary significantly, the common theme is office space vacancy caused by weaker demand and high construction activity. Consultants predict that the largest supply will be in Greater China. However, the largest rent reductions are expected in developed Asia-Pacific markets. (In Asia-Pacific countries, new supply for 2020-2022 represents 15.3% of 2019 vacant space; in emerging markets it is 23.0%; and in Greater China it is 26.0% of 2019 vacant space).

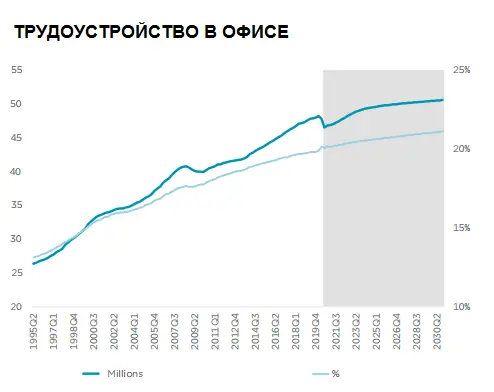

In the West, supply peaks will be reached in 2021 and 2022, but construction levels at the start of the COVID-19 recession were generally more modest than in earlier periods. Consultants do not confirm the thesis that lower demand in Canada, Europe, and the US leads to a structural increase in vacancy. Demand recovery will be gradual from the early to mid-2020s until business revival begins in Europe and North America. It is the balance of supply and demand combined with the overall state of the economy in each scenario that determines the expected rent trajectory.

EUROPE

BASE SCENARIO: PROBABILITY 50%

The base scenario for Europe assumes job losses of 1.2 million working-age population in 2020, which is 0.9 million more jobs lost than in 2008-2010 due to the Global Financial Crisis. Considering only this factor, demand in the European office sector is forecast to shrink by 39.4 million sq. ft. (1.1% of total space) over the next two years, with the majority of this (-29.1 million sq. ft.) occurring in 2021. An additional -5.8 million sq. ft. will be thrown onto the market from coworking in the coming years, assuming only 10% of coworking space returns to the market.

Cyclical factors are the main obstacle to recovering demand for office space in the short term, accounting for approximately 80% of office space that will come to market over the next 2 years. The increased share of remote work is expected to reduce the need for offices by an additional 10.2 million sq. ft. during 2020-2021. As a result of the impact of cyclical and structural factors on the office real estate sector, 57.9 million sq. ft. of space will come to the European market as a whole. Positive demand in the first nine months of 2020 and the second half of 2022 reduces the magnitude of annual figures for these years.

Regarding supply, office construction completion in Europe is scheduled for 2020-2021, facilitated by high pre-leasing activity in recent years. New space growth averaged only 1.2% of growth for the 2010-2019 period due to stricter financing requirements arising from the last crisis. But growth will be 1.5% in 2020 and peak at 2.1% in 2021.

The simultaneous reduction in demand and increase in new supply leads to an increase in vacant space share from the historical low of 0.9% in Q4 2019 to a peak of 10.6% by Q1 2022. The peak vacancy level corresponds to, but slightly exceeds, the peak vacancy level of 10.2% recorded in Q4 2009. Thus, prime rent is expected to decline by 10.7% from peak to minimum, corresponding to the 10.6% decline during the Global Financial Crisis, but less than the 13.4% decline after the Dot Com bubble. By the end of 2024, prime segment rent will return to pre-crisis levels.

In 2022, demand for office space will again exceed supply, driven by labor market improvement. Employment is expected to reach pre-crisis levels by Q3 2022, representing a 10-quarter recovery period compared to the Global Financial Crisis period. Office space demand will peak in 2023, as annual employment growth slows. Developers will respond by keeping new construction at or below 1% of total space. In the long term, both demand and supply will adapt to slower workforce growth and structurally lower, albeit demographically driven, office job growth.

The reduction in demand for office space due to remote work share will be greatest by 2023-24, as the share of remote employees increased significantly in the first half of the 2020s. However, the reduction in cyclical factors will lead to a decrease in available space for rent from 10.6% in early 2022 to a minimum of 7.0% by mid-2025. This is higher than pre-pandemic but lower than in 2006-07, after a more significant demand drop and shorter recovery phase following the Dot Com collapse.

Demand in European offices is expected to be 17.4% lower compared to 2022-2030 due to increased remote work and short-term coworking issues, with most of this adjustment occurring from 2021 to 2024. Additionally, if the share of permanent remote work increases by only half the amount assumed in the base scenario (to 8.0% vs. 10.6%), then the net demand impact for 2022-2030 will only be 10.6% lower than otherwise. Any reduction that occurs in the near future or permanently will also act as a standard.

Europe is a diverse region where some countries and office markets are more likely to experience stronger structural shifts due to increased remote work than others. We assess the propensity for remote work in major European cities using a weighted index equal to six q.

Cities like London and Paris rank highest, indicating that these office markets may achieve a higher relative share of remote work than others, driven by higher housing prices, longer commute times, greater population density, and wider adoption of work from home.

Generally, the UK has a higher propensity for remote work due to the following factors: higher job density compared to most of Europe, a significant share of the population working from home, and a large employment sector.Nordic countries also rank high due to wider adoption of work from home (pre-COVID) and a large share of ICT (information and communication technology) employment. At the lower end of the range are several markets in Central and Eastern Europe, Italy, Spain, Portugal, and Benelux countries, which generally have smaller populations, lower population density, lower share of remote employees, and lower job density.

OPTIMISTIC SCENARIO: PROBABILITY 10%

Key assumptions- In 2020, 0.9 million people will be cut from offices in Europe. However, with rapid recovery, average annual office job growth will be 356,000 jobs from 2021 to 2030.

- Initially, the European Central Bank (ECB) keeps interest rates unchanged despite the rollback and supports recovery with large asset purchases and further LTROs

- Eurozone governments introduce additional overall economic support, improving the institutional infrastructure of countries

- Economic activity declines less and recovers earlier than in the base scenario, leading to a higher long-term GDP level

- The combined impact of cyclical and structural factors leads to 42.1 million sq. ft. coming to market during 2020-21. Vacant space share peaks at 10.2% in early 2022 and gradually declines to a minimum of 7.0% by early 2025. From 2020 to 2022, prime sector rent will fall from peak to minimum by 8.7% and return to pre-crisis levels by 2025.

PESSIMISTIC SCENARIO: PROBABILITY 10%

Key assumptions- In 2020, 1.8 million people will be cut from offices in Europe. Annual job growth averages 416,000 people from 2021 to 2030, with delayed but strong recovery in 2022 and 2023, when more than one million jobs will be added annually

- A sustained period of low investment in innovative industries and human capital puts pressure on productivity growth, undermining economic potential

- The combined impact of cyclical and structural factors leads to 95.4 million sq. ft. of space coming to market in 2020-2021. Vacant space share will peak at 12.3% at the end of 2022 and then gradually decline to 7.3% by 2025. From 2020 to 2022, premium sector rent will fall from peak to minimum by 16.3% and return to pre-crisis levels by 2028