One of the most talked-about bills 5600 was adopted by the Verkhovna Rada and signed by the President.

In the people, this Law is called “resource” or “anti-Akhmetov” due to the increase in rent rates on iron ore.

Regarding real estate, this Law changes the rate and principle of paying tax on income from sale.

Who was affected by the changes?

We immediately want to reassure that the tax benefit for those who owned property (apartment, private house...) for more than 3 years is preserved.

We also note that changes will not affect non-residents, for whom the tax rate is already high - 18%. Changes apply to those who sell two or more real estate objects per year.

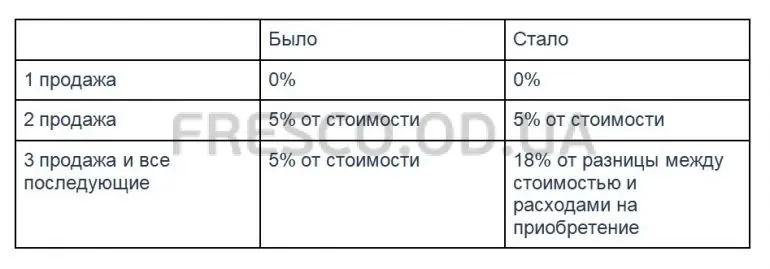

How has the rate changed?

For sellers whose first sale in the year is property they owned for more than 3 years

For sellers who do not fall under the three-year ownership benefit, tax rates will be as follows:

We want to note that if the owner of the first sale in the year sells an apartment they owned for 2 years, and then sells an apartment they owned for 4 years, then despite the ownership period, tax will be levied.

When selling commercial real estate, apartments, the rate will also be 18% from the second sale.

By the way, in our article

Taxes on apartment and apartment sales we detailed the taxes that all parties to the purchase-sale transaction must pay.

How has the approach to tax calculation changed?

We want to draw attention to the fact that 18% is paid not from profit, as the media have been presenting it lately, but from income. Moreover, such income can be reduced by the amount of

documented expenses.

In case of reducing income by the amount of expenses, the seller will have to file a declaration and attach documents confirming such expenses by the end of the calendar year.

What are acquisition expenses?

The list of possible expenses is quite large; we will list the main most common ones:

- Expenses under the purchase-sale contract for real estate (relevant for those who bought “secondary” property)

- The cost of the object under the exchange agreement (relevant for those who exchanged for “secondary” property)

- Money paid for securities or property rights that were later converted into a real estate object (relevant for those who bought a new building)

- Money transferred to the manager of the Construction Financing Fund FFC (relevant for those who bought a new building through FFC)

- Expenses for constructing a real estate object (relevant for those who individually built an individual residential house or participated in construction, for example, a cottage settlement or townhouses)

How to confirm acquisition expenses?

We want to draw attention to how the term expenses is presented for those who bought a new building. Expenses are the money that was paid.

That is, to confirm such expenses it will be necessary to attach, for example, bank statements, receipts of cash receipt orders, or other documents confirming the fact of payment.

Therefore, it is now important to keep these documents.

How will the tax amount change?

Depending on what the initial expenses were,